What are continuous controls for outgoing payments? A 2026 finance leader's guide

Fewer fraud losses, faster vendor onboarding, and a continuous audit trail: what we mean when we talk about “traditional controls,” how fraudsters are exploiting them, and why accounts payable (AP) processes need their own version of continuous control monitoring.

Why this matters to finance leaders right now

If you're running an AP function in 2026, you're probably watching a familiar pattern. Fraud attempts are getting more convincing. Manual checks are getting harder to defend in a board meeting. Auditors are starting to ask different questions.

Eftsure's 2026 Australian payment security research bears it out: 52% of finance teams faced a fraud attempt in the past twelve months, 90% say AI-era scams are harder to detect than traditional fraud, and 91% don't believe senior leaders fully understand payment fraud. For broader Australian payment fraud trends, including ACCC and National Anti-Scam Centre data, see Eftsure's Payment Fraud Index.

Continuous controls are the model finance leaders are moving to. They sit inside the AP workflow and verify every vendor and every payment continuously across six independent layers, replacing a patchwork of manual callbacks, partial-match bank-side checks, and once-a-year vendor reviews.

The gain is concrete. Fewer fraud incidents reaching the payment stage. Faster vendor onboarding because verification runs automatically rather than as a manual queue. Less time spent verifying low-risk payments by hand. A continuous audit trail that maps cleanly to APRA CPS 230 in Australia and SOX-aligned segregation of duties in the US.

What you'll get from this guide

A working answer to four questions your team, your CFO, and your auditors keep asking:

What are continuous controls in plain language, with an example you can point to?

How do they differ from single-layer controls (Confirmation of Payee, manual callbacks) and point-in-time controls (annual reviews, onboarding-only checks)?

What does an implementation look like inside an AP function, including the first 90 days?

What questions should you ask when evaluating any continuous controls approach, whether you build it, buy it, or assemble it from a mix?

A note on terminology: payments versus IT continuous controls

If you've searched "continuous controls" recently, you'll have seen two very different things in the results. One is about IT and compliance: continuous controls monitoring (CCM), automated checks against access controls, configuration drift, SOX-aligned IT general controls, and audit readiness. The other is about payments: continuous verification of vendors, bank details, sanctions exposure, and the integrity of every payment that leaves the business.

Both use the same words. They solve different problems.

The IT and GRC version focuses on the state of your systems. The payments version focuses on the integrity of your money flow. They overlap in regulated environments (think APRA CPS 230, where third-party risk and operational resilience cut across both), but the operating model, the team that owns it, and the tools involved are different.

The parallel in naming is deliberate. In the same way that we've borrowed the cybersecurity concept "red teaming" to help finance functions pressure-test their workflows and systems, finance leaders have borrowed the language of continuous controls because the architecture pattern is the same: automated, layered, persistent checks that replace point-in-time manual ones. As payment fraud risk has escalated, finance functions have realised that the controls model that works for IT compliance also works for the protection of outgoing money.

This guide is about the payments meaning. From here on, "continuous controls" refers to controls that safeguard payments.

What are continuous controls for outgoing payments?

Continuous controls for outgoing payments are a set of independent, automated verification layers that run throughout the procure-to-pay cycle, every time a vendor is added, changed, invoiced, or paid. They sit inside the AP workflow rather than alongside it, and they're designed to give finance teams an evidence-backed answer to a single, recurring question: are we paying the right party, by the right method, for the right reason, today?

Three properties define them.

They're continuous, not point-in-time.

A traditional control fires at one moment: vendor onboarding, an annual review, a manual callback before a payment release. A continuous control fires every time the state of the world changes. New vendor? Verify. Bank detail change? Re-verify. New invoice with revised payment instructions? Verify against the previous record. Quarterly sanctions screen? Replace with persistent monitoring that flags new sanctions exposure within hours of a list update. The cadence question stops being "when did we last check?" and becomes "are we checking everything, all the time?"

They're multi-layered, not single-layer.

A single-layer control verifies one fact about a vendor or payment. Most named industry controls (Confirmation of Payee, penny drops, manual callbacks, bank-side name matching) are single-layer. Each is useful in isolation, but each leaves blind spots. A multi-layered control stacks independent checks: business identity, bank account ownership, sanctions exposure, behavioural anomalies, community fraud signals, and human expert review of edge cases. The architecture compounds: each layer covers a different failure mode, and the combination is materially stronger than the strongest individual layer.

They're workflow-embedded, not bolt-on.

A continuous control isn't a separate audit step or a parallel system. It runs inside the AP workflow, between the existing vendor master file, the ERP, the AP automation tool, and the bank. From the AP team's point of view, the controls operate in the background and surface only when something needs attention. The intent is to remove the manual verification burden from people who are already stretched, not to add another approval layer to a process that's already too slow.

What continuous controls don't do is replace the rest of your financial control environment. Segregation of duties, dual authorisation, vendor master file governance, payment approval workflows: all of those remain. Continuous controls extend the environment by giving each of those controls something to act on, namely an evidence-backed view of who you're paying and whether anything material has changed since the last time you checked.

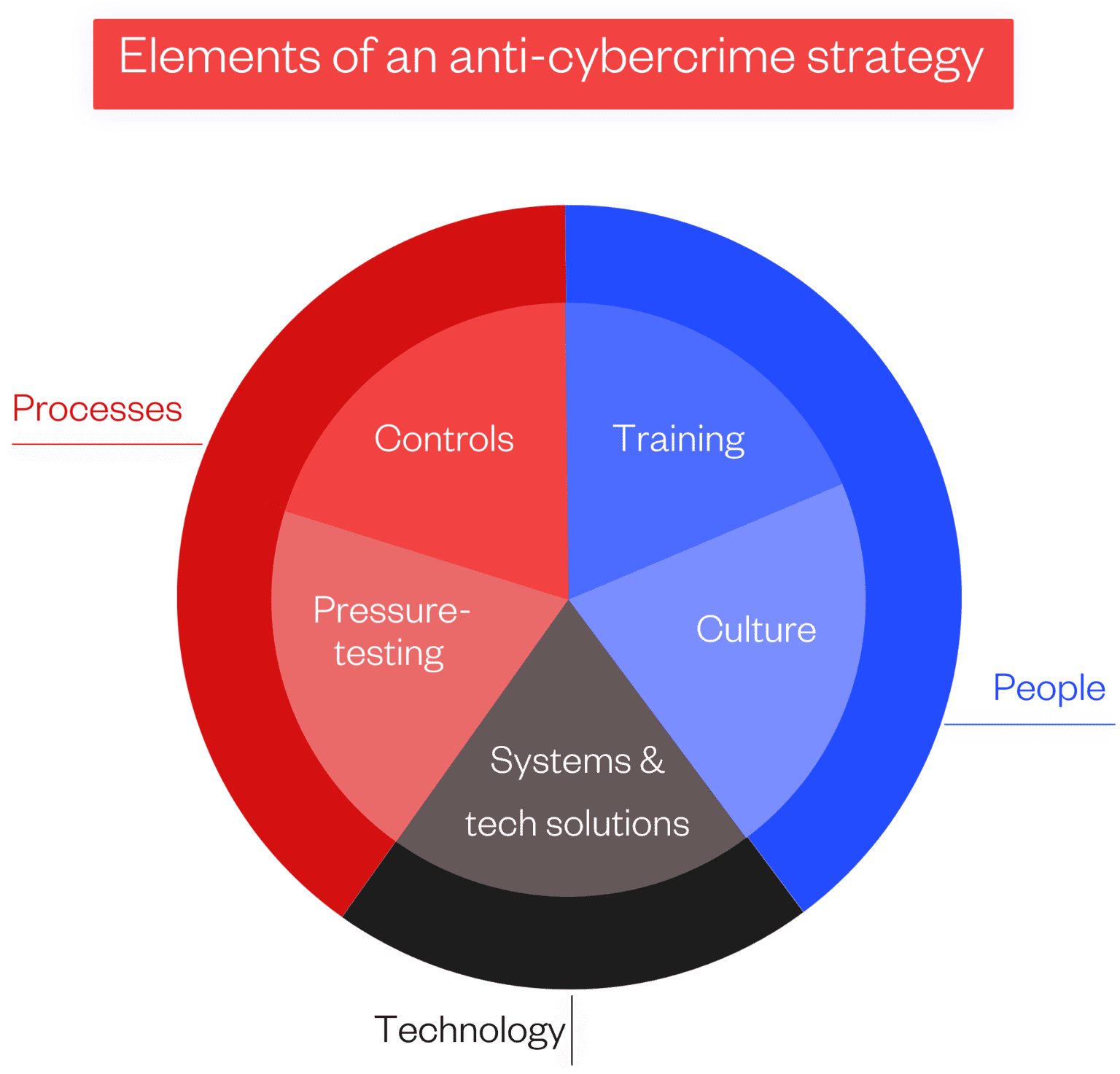

Why continuous controls matter in a modern anti-cybercrime strategy

The case for continuous controls starts with a distinction many organisations still treat as semantic but is actually structural. Cybersecurity protects systems and data. Anti-cybercrime protects money. They sound similar, but they reach different conclusions about who needs to own them and what the controls should look like.

We've covered the importance of an anti-cybercrime strategy and why CFOs should lead it. The short version: cybercriminals attacking finance functions aren't usually trying to steal data, they're trying to redirect money.

The skills, controls, and ownership model that protect data don't automatically protect cash flow. Finance leaders are best placed to lead an anti-cybercrime strategy, and the five elements that make one effective (training, culture, internal controls, pressure testing, and technology) cut across both functions.

Continuous controls are the operational expression of the internal controls element. They're the layer that makes everything else hold under modern fraud conditions.

The reason traditional controls have started to fail is pretty straightforward: manual checks were built for a world where attackers were slow, working in isolation, or prone to obvious errors. Phishing emails were riddled with spelling mistakes. Voice impersonation took skill and rehearsal. Vendor email compromise was rare because hijacking an inbox at scale was hard.

None of those conditions hold today.

Generative AI has changed the economics of fraud. A convincing impersonation email now takes minutes to produce. Voice cloning is available off the shelf. Eftsure's 2026 Australian payment security research found that 90% of respondents believe AI scams are harder to detect than traditional fraud, and 52% had experienced a fraud attempt in the past twelve months. The 91% of respondents who don't believe senior leaders fully understand payment fraud tells you something about the awareness gap inside organisations, too.

In this environment, three traditional control failures show up repeatedly.

A vendor callback to a number on a recent invoice reaches the fraudster, not the vendor. The check confirms the change, and the payment goes out.

A bank-side name match returns a partial match, and the AP team makes a judgement call under time pressure. The judgement is wrong because the impersonated entity was registered with a near-identical name three weeks earlier.

An onboarding check confirms a real business with real bank details at the time of onboarding. Six months later, the bank details change. The change is processed without re-verification because the vendor is already on the master file.

Each of those failure patterns has a continuous-controls answer. The callback failure is addressed by independent verification of the vendor's contact records before the callback, plus a check against community fraud signals. The bank-side name match failure is addressed by stacking identity and ownership checks rather than relying on a single match score. The dormant vendor failure is addressed by event-triggered re-verification on every change.

The role of continuous controls in AP workflows

To make continuous controls concrete, it helps to walk the AP lifecycle from end to end and look at where fraud risk shows up and what continuous controls do at each touchpoint.

A typical accounts payable lifecycle has six stages: vendor onboarding, master file maintenance, invoice processing, payment release, reconciliation, and audit.

Vendor onboarding. The riskiest moment in the lifecycle. A new vendor record is created and any error or impersonation here becomes structural: the bad data persists until something catches it. Traditional controls at this stage rely on documentation review (an ABN search, a void cheque, a manually verified phone call) and on the assumption that the onboarding moment is a good moment to verify. Continuous controls at onboarding do three things differently. They verify the business identity against authoritative sources rather than supplied documentation. They verify bank account ownership independently of the documents the vendor provided. And they check the proposed vendor against community fraud signals and sanctions lists before the record is committed to the master file.

Master file maintenance. The master file is one of the most attractive targets in the AP environment because a single record change can redirect every future payment. Continuous controls operate as a persistent layer here. Any change to bank details, contact information, address, or banking authority triggers a verification event. Dormant vendors that suddenly become active are flagged for re-verification. Records are monitored for sanctions list updates, ownership changes, and adverse media. Where traditional controls treat the master file as a static reference, continuous controls treat it as a living dataset that can drift out of integrity at any time.

Invoice processing. Most invoice fraud sits in the gap between the invoice arriving and the payment being approved. A fraudulent invoice that uses a real vendor's branding, references a real PO, and asks for payment to a slightly different bank account is hard to catch with manual review. Continuous controls cross-check invoice payment instructions against the verified record on file, flag any drift between the invoice details and the master record, and surface unusual instructions (urgency claims, last-minute changes, requests to skip standard approval routes) for review.

Payment release. The last opportunity to stop a fraudulent payment before money leaves. Continuous controls verify the payee details one final time at release, check for any changes since approval, and run anomaly detection across the batch (unusual amounts, unusual patterns, payments that don't match purchase order history). This is also where segregation of duties and dual authorisation work most effectively, because they're operating on payments that have already been verified at every prior stage.

Reconciliation. Continuous controls keep producing evidence after the payment has left. Every verification, every decision, every override is logged with a timestamp and a reason. Reconciliation against bank statements can be cross-referenced against the verification record, which makes anomalies easier to spot and investigation faster.

Audit. This is where continuous controls earn back the implementation work. Every step of every payment has a documented evidence trail. Auditors don't need to ask "how do you verify vendors?" and accept a process description. They can ask "show me the verification record for these payments" and get an answer in minutes.

The bigger shift this represents is in how the AP team sees itself. Under a traditional control model, AP is the last line of defence. Every payment is something the team has to actively defend against fraud. Under a continuous controls model, AP is the operator of a controlled system. The defence is built into the workflow, and the team's attention goes to the exceptions the system surfaces rather than to defending every transaction individually.

How continuous controls work: the verification layers

Continuous controls aren't a single technology. They're an architecture made up of independent verification layers that each address a different fraud vector. Understanding what each layer does, and why no single layer is sufficient, is the first step in evaluating any continuous controls approach.

There are six layer types finance leaders should expect to see in a credible continuous controls implementation.

Layer 1: Identity verification

The check that the business you're paying actually exists and is who it claims to be. At its simplest, this involves verifying the business registration (an ABN or NZBN in Australia and New Zealand, an EIN in the US) against the authoritative registry. A serious implementation goes further: it verifies trading names against the registered entity, checks beneficial ownership, confirms tax compliance status, and flags any recent changes to the corporate record. The failure mode this layer addresses is a fraudster impersonating a real business with a registered-but-shell entity that has a near-identical name.

Layer 2: Bank account ownership verification

The check that the bank account you're about to pay actually belongs to the named business. This is the layer that named services like Confirmation of Payee and bank-side name matching partially address. The "partially" matters. A name-match check returns a score, not a verification. The score can be a close match, a partial match, or a no-match, and at the partial-match end of the spectrum, the AP team makes a judgement call. A continuous controls implementation treats bank account ownership as a verified fact, not a match score, and combines bank-side checks with independent registry data, banking authority records, and community intelligence. The failure mode this layer addresses is the bank account opened to launder payments under a name designed to score a partial match.

Layer 3: Sanctions, PEP, and adverse media screening

The check that the entity you're paying isn't on a sanctions list, isn't a politically exposed person with risk implications for your business, and doesn't have adverse media that should trigger an additional review. This layer has been standard in financial crime compliance for decades, but continuous controls run it persistently rather than at onboarding only. New sanctions designations and adverse media events trigger re-screening across the existing vendor file. The failure mode this layer addresses is an entity that was clean at onboarding becoming a sanctions exposure six months later without anyone noticing.

Layer 4: Behavioural and anomaly detection

The check that the payment you're about to send looks like the payments you've sent before, or that any deviation has a defensible reason. This is the layer where pattern recognition and machine learning do useful work. Unusual amounts, unusual frequencies, unusual payment timing, instructions that deviate from historical pattern, requests to change payment methods: all are signals that something is worth a closer look. The failure mode this layer addresses is a fraudster who has compromised a real vendor's email and is submitting a request that looks plausible at the document level but doesn't match the vendor's historical behaviour.

Layer 5: Community or network signals

The check that the vendor, the bank account, the contact details, or the patterns associated with this payment haven't been flagged elsewhere. Where a single organisation sees only its own fraud attempts, a network of organisations sharing signals sees patterns much earlier. A phone number associated with a recent attempted scam at another organisation, a domain registered three days before an invoice was issued, a bank account that has appeared in two unrelated fraud cases this month: each is a strong signal. The failure mode this layer addresses is a fraud pattern that's already been seen elsewhere but is new to your organisation.

Layer 6: Expert analyst review

The check on the edge cases that automated layers can't resolve. Continuous controls do most of the work in the background, but a small share of cases sits at the boundary where automated logic isn't sufficient. A human analyst, looking at the full picture of a vendor's record, can make calls automated systems can't. The failure mode this layer addresses is the sophisticated fraud that succeeds precisely because it sits in the grey area between automated rules.

The architectural point is that no single layer covers every failure mode, and the combined coverage is greater than the sum of the parts. A continuous controls implementation that includes only two or three layers leaves predictable gaps. Six layers, each independent, is the working baseline for an enterprise environment.

Examples of continuous controls in accounts payable

If "continuous controls" still feels abstract, here are concrete examples of what they look like in practice. Each runs automatically inside the AP workflow, without adding manual steps to the team's day.

Vendor identity verification on every new vendor. When a new vendor is added to the master file, the system independently verifies the business registration (ABN or NZBN), checks trading names against the registered entity, and flags shell entities with near-identical names to legitimate vendors.

Bank account ownership verification on every change. Any time a bank detail changes, the system verifies that the named business actually owns the account, rather than relying on a partial name match or supplied documentation.

Persistent sanctions and adverse media screening. Rather than screening only at onboarding, the system continuously monitors every vendor against sanctions list updates, politically exposed persons, and adverse media. New designations trigger automatic re-screening across the file.

Duplicate payment detection. Every payment is cross-checked against recent payment history for matches on amount, invoice number, vendor name, and bank account combinations that suggest a duplicate. A duplicate flagged before release is a loss prevented.

Vendor master file change monitoring. Bank detail edits, banking authority changes, contact updates, and dormant-to-active reactivations all trigger a verification event. The master file is treated as a living dataset, not a static reference.

Payment-time anomaly detection. Behavioural models compare the current payment against the vendor's historical pattern. Unusual amounts, unusual timing, instructions to skip standard approval routes, and last-minute changes all surface for review.

Community fraud signal checks. Phone numbers, domains, and bank accounts associated with fraud at other organisations are flagged before they make it into your records. Patterns one organisation sees once, the network sees many times.

Continuous evidence logging. Every verification, flag, override, and decision is logged with a timestamp and a reason, ready for internal audit and external assurance.

A useful question for finance leaders is: which of the existing AP controls in your environment should be monitored continuously rather than at a periodic cycle? In most cases, the answer is all of the controls that touch a record that can change without warning: vendor identity, bank account ownership, sanctions exposure, and payment instructions. Anything tied to a record whose state can drift is a candidate for continuous monitoring.

Single-layer versus multi-layered controls

The most useful contrast for finance leaders evaluating continuous controls is the contrast between single-layer and multi-layered approaches. Most existing payment fraud controls, in most organisations, are single-layer. To fully understand continuous controls, let's dig into common types of single-layer controls, as well as what they can offer (and what gaps they might leave behind if used as a standalone defence).

A single-layer control verifies one fact about a vendor or a payment. The most common examples sit in four categories.

Account name checking. A check that the name on the bank account matches the name on the payment instruction. Useful in the right circumstances and now widely available in Australia.

What it does well: confirms that a bank account is in the name expected.

What it doesn't do: confirm the business is real, confirm the entity is tax-compliant, confirm the contact is who they say they are, confirm the account wasn't opened under a near-identical name to launder payments, or cover cross-border payments where the scheme doesn't reach.

Penny drops and micro-deposit verification. A small test deposit that confirms an account is live and can receive funds. Useful for cross-border setup where name-match infrastructure doesn't exist.

What it does well: confirms account operability.

What it doesn't do: tell you anything about the identity or legitimacy of the account holder.

Manual vendor callbacks. A phone call to the vendor to confirm bank details before a payment or a change. Useful as a control of last resort when nothing better is available.

What it does well: introduces a human verification step.

What it doesn't do: protect against the very common case where the contact details on file have been modified by the fraudster, the AI-generated voice on the other end of the line is convincing, or the genuine vendor has been compromised and is now part of the attack.

Bank-side fraud monitoring. Checks the bank runs at payment release. Useful as a final filter.

What it does well: catches some patterns the bank has visibility on.

What it doesn't do: cover the period before the payment reaches the bank (which is where most of the controllable risk sits), tell you anything about the vendor record on your master file, or share signals across organisations.

Each of these controls is useful. The problem is structural. Each verifies one fact, in one moment, against one source. Fraud that targets the gaps between them succeeds reliably.

A multi-layered control architecture is different. It treats verification as a problem of stacking independent checks so that no single fact, source, or moment carries the full weight of the decision. The pattern is well established in security work generally: defence-in-depth. No single layer is expected to be perfect. The combined coverage is what matters.

The practical differences between single-layer and multi-layered approaches sit across five dimensions.

Dimension

Single-layer controls

Multi-layered continuous controls

Coverage

Confirms one data point (usually the account name).

Verifies business identity, bank account ownership, sanctions exposure, behavioural patterns, community fraud signals, and edge-case expert review across the full procure-to-pay lifecycle.

Cadence

Point-in-time. Runs at onboarding, at payment, or at periodic review.

Continuous. Every new vendor, every change to an existing record, every payment is independently verified.

Geography

Often domestic only. Schemes like Confirmation of Payee don't cover cross-border payments.

Domestic and cross-border, including international wire

Outcome

A match score or a yes/no result. The AP team makes the judgement call when results are ambiguous.

A documented verification record across every layer. The AP team acts on exceptions rather than evaluating every transaction.

Failure mode

Bad bank details can enter the master file and persist undetected. Losses happen before AP sees them.

Verification happens before records enter the master file. Anomalies surface in time to act on them.

The honest answer about when single-layer controls are acceptable is that they often work in low-risk, low-value, low-complexity environments. A small business paying a handful of well-known vendors with predictable patterns can run single-layer controls and rarely encounter their limits. The threshold at which multi-layered becomes essential is when value, complexity, or regulatory expectations rise: enterprise-scale payment volumes, multi-entity structures, cross-border activity, large or fast-changing vendor masters, regulated industries with specific obligations around third-party risk, or any environment where a single fraudulent payment could represent a material loss.

For most organisations above the small-business threshold, the question isn't whether single-layer controls are useful (they are) but whether they're sufficient on their own (they aren't).

Point-in-time versus continuous controls

The second contrast finance leaders should understand is point-in-time versus continuous. It's related to the single-layer versus multi-layered distinction but separate from it. A control can be multi-layered and still point-in-time. A control can be single-layer and still continuous. The two dimensions are independent.

Point-in-time controls run when a specific event occurs, then stop until the next event. The most common examples are onboarding verification (we check the vendor when they're added, then trust the record), periodic vendor reviews (we re-verify the vendor master annually), and audit-cycle attestations (we confirm controls are working at audit time).

Point-in-time controls fail for three reasons that are well-known to anyone who's run AP at scale.

First, the world changes between checkpoints. Vendor bank details change. Contacts leave. Companies are acquired, sold, restructured, or fail. The record that was verified at onboarding becomes unreliable within months and dangerously stale within a year or two. Most fraudulent changes to vendor records happen between the periodic review cycles, not at them.

Second, attackers time their attacks to the gaps. A fraudster who has compromised a vendor's email knows that bank detail changes will be processed without re-verification because the vendor is already on the master file. The window between the change and the next scheduled review is the attack window.

Third, the audit signal is weak. Point-in-time evidence shows that a control was working at a specific moment, not that the control has been working continuously. Auditors and regulators are increasingly distinguishing between the two.

Continuous controls behave differently. They treat the integrity of the record as something that can decay, and they re-verify on three triggers: when the record changes, when an external signal warrants re-verification, and when a payment is about to happen. The shape of the cadence matters.

Event-triggered verification runs when something on the record changes (a bank detail update, a contact change, a banking authority change). It's the most common form of continuous behaviour, and it closes the most obvious attack window.

External-signal verification runs when something outside the record changes (a sanctions designation, an adverse media event, a community fraud signal flagging the vendor). This is where continuous controls extend beyond the organisation's own data.

Payment-time verification runs at the moment a payment is about to be released. It catches changes that happened in the gap between approval and release, and it provides the final evidence point for audit.

Together, these three triggers produce a continuous evidence trail rather than a series of disconnected attestations. For audit and regulatory assurance work, this matters. APRA CPS 230 in Australia, FedRAMP and SOX-aligned segregation of duties in the US, and the broader operational resilience agenda globally all push in the direction of continuous evidence rather than periodic attestation. Continuous controls are the operational answer to that regulatory direction.

How to implement continuous controls in your AP function

This is how finance teams automate fraud controls in practice. Implementing continuous controls in an AP function isn't a single project. It's a programme that runs across systems, processes, and people, with a sensible sequence that depends on where the function is starting from.

A useful implementation framework has five steps.

Step 1: Assess

Map your current controls against the AP lifecycle. At each stage (onboarding, master file maintenance, invoice processing, payment release, reconciliation, audit), document what control exists, what failure modes it covers, and what gaps remain. The deliverable is a heat map of where the existing controls hold and where they don't. This is the work that justifies the implementation budget, and it's also the work that surfaces the quick wins.

Step 2: Design

Decide which layers go in where. Most organisations land on the same answer: identity verification and bank account ownership verification at onboarding and on every change; sanctions screening as a persistent layer across the file; behavioural and anomaly detection at payment time; community signals across all stages; expert review for edge cases. The design step also covers integration: where the controls plug into the ERP, AP automation tool, and banking infrastructure. Most enterprise environments will need integrations with SAP, NetSuite, Workday, Oracle, Dynamics 365, or Sage Intacct.

Step 3: Integrate

Connect the verification layer to the systems where the AP team already works. The principle is no rip-and-replace. The continuous controls layer sits between the vendor master file, the ERP, the AP tool, and the bank, and surfaces its outputs in the existing workflow rather than requiring the team to learn a new interface. Implementation time varies, but a well-integrated implementation should be live in weeks for a mid-market organisation and within a quarter for a complex enterprise environment.

Step 4: Operate

Define the governance model. Who owns the controls (finance, typically, with IT and risk in support)? What's the escalation path when an exception is raised? Who can override a flag and what evidence is required? How does the segregation of duties model interact with the new controls? The operating model is where most implementations either succeed or stall. The technical integration is the easier half of the work.

Step 5: Audit

Build the reporting and evidence flow from the start. Every verification, every flag, every override is logged. Reports to internal audit and external assurance teams should be standing outputs of the system, not custom requests. This is also where the regulatory alignment gets demonstrated. APRA CPS 230 in Australia and SOX-aligned controls in the US both benefit from the kind of continuous evidence trail that the system produces by default.

A useful sequence for the first 90 days: remediate the vendor master file (clean the data the controls will operate on), implement onboarding controls (so no new bad data enters), then implement payment-time controls (so existing exposures are caught before money moves). Master file maintenance, behavioural detection, and community signal integration follow in the next quarter. The order matters. You want the inflow stopped before you start the deep clean.

Continuous controls checklist

When evaluating any continuous controls approach (whether built in-house, bought from a vendor, or assembled from a mix), the same set of questions surfaces what matters. Use this as a working checklist.

Coverage. Does the approach verify business identity, bank account ownership, sanctions exposure, behavioural patterns, community signals, and edge-case expert review? If one or more of these layers is missing, what failure modes does that leave open?

Cadence. Does verification run at every stage of the AP lifecycle (onboarding, master file changes, invoice processing, payment release)? What triggers re-verification on an existing record? How long is the maximum window between an external change (a sanctions designation, an adverse media event) and a re-verification trigger?

Outcome. Does the approach produce a documented verification record for every vendor and every payment, or does it produce match scores that require human judgement? Are the records retained in a form that's audit-ready by default?

Integration. Does the approach integrate with the AP team's existing systems, or does it require a parallel workflow? Which ERPs and AP tools is it certified against? What's a realistic implementation timeline for a function of your size?

Audit and assurance. What evidence does the approach produce for internal and external audit? How does it support APRA CPS 230, SOX-aligned segregation of duties, or other regulatory frameworks that apply to your organisation? Is the evidence produced as a standing output or as a custom request?

Geography. Does the approach cover cross-border payments with the same depth as domestic ones? Which banking consortiums and registries does it integrate with internationally?

Governance. What's the operating model? Who owns the controls, who escalates exceptions, and what overrides are permitted and logged? Does the approach assume an AP team of one or fifty, or does it scale?

Failure modes. What does the provider say happens when a verification fails (a vendor turns out to be fraudulent, a payment is processed despite a flag, a sanctioned entity makes it through)? Is there a guarantee or coverage commitment, and what are its terms?

The pattern these questions reveal is that continuous controls form an architecture, not a feature. The questions that matter are about the architecture's coverage, cadence, evidence, and integration, not about marketing claims.

Frequently asked questions

What's the difference between continuous controls for payments and continuous controls monitoring (CCM)?

CCM is the IT and compliance practice of automating monitoring against system controls (access management, configuration, SOX-aligned IT general controls). Continuous controls for payments is the finance practice of automating verification of vendors, bank details, and payments. The architectural pattern (automated, layered, persistent checks) is similar. The risks they address are different. CCM addresses the integrity of your systems. Continuous controls for payments address the integrity of your outgoing money.

Do continuous controls replace internal audit?

No. Continuous controls give internal audit something stronger to work with. Audit teams move from sampling-based reviews of whether controls worked to evidence-based confirmation that controls are working. The audit function still owns assurance, but the evidence base is continuous rather than periodic.

How are continuous controls different from KYC?

KYC is mostly an onboarding-stage check focused on regulatory obligation: customer due diligence, anti-money-laundering checks, sanctions screening at the start of a relationship. Continuous controls extend the KYC mindset across the lifecycle and adapt it for outgoing payments (sometimes referred to as Know Your Payee or KYP). The same disciplines that financial services applies to incoming customers, finance functions apply to outgoing vendors.

How do continuous controls interact with bank-side fraud monitoring?

Bank-side monitoring sits as one layer in the stack. It catches some patterns the bank has visibility on (often after the payment has left), but it's a single-layer, point-in-time check. Continuous controls add the verification work that happens before the payment reaches the bank, which is where most of the controllable risk sits, and they monitor for changes that bank-side checks don't see.

Where do continuous controls sit in relation to segregation of duties?

Segregation of duties is a process control. Continuous controls are an evidence layer. They complement each other. Segregation of duties governs who can do what (a preparer cannot approve, an approver cannot release). Continuous controls govern what the underlying facts actually are (is the vendor real, is the bank account theirs, has anything changed). A strong AP environment needs both.

Can mid-market finance teams implement continuous controls, or is this enterprise-only?

Mid-market implementation is the common case, not the exception. The architecture works at any scale. The implementation effort scales with the complexity of the integration environment (more ERPs, more entities, more currencies) rather than with the size of the AP team. Mid-market teams often see the largest relative gains because they have the same fraud exposure as enterprise teams without the headcount to staff manual controls.

How do you catch duplicate payments?

Duplicate payment detection sits inside the payment-release layer of a continuous controls architecture. Every payment about to leave is cross-checked against recent payment history for matches on amount, invoice number, vendor name, and bank account. Where traditional controls catch duplicates after the fact in reconciliation, continuous controls catch them before money moves. The check is automatic, so the AP team only sees the cases that need human judgement.

How do you monitor vendor changes?

Continuous controls treat the vendor master file as a living dataset. Any change (bank details, banking authority, contact information, address, ownership) triggers a verification event before the change is committed. Dormant vendors that suddenly become active are flagged for re-verification. External signals like a sanctions designation or an adverse media event also trigger re-verification, even when nothing on the record has changed internally.

How do you know your controls are actually working?

Continuous controls produce evidence as a default output. Every verification, every flag, every override, and every decision is logged with a timestamp and a reason. Where periodic controls leave you with a process description, continuous controls leave you with a record. Reports to internal audit and external assurance should be standing outputs of the system, not custom requests, and a serious implementation will let you query the evidence at vendor, payment, or batch level.

Continuous controls vs periodic audits: what's the difference?

Periodic audits sample the control environment at a moment in time, usually quarterly or annually. They confirm that the process existed and was followed during the sample window. Continuous controls verify the underlying facts in real time, across every vendor and every payment. The two work together. Periodic audit gives you assurance that the design is sound. Continuous controls give the audit something to test against. A continuous controls implementation makes the audit easier and the evidence stronger, but it doesn't replace the assurance function.

Why do monthly audits miss fraud signals?

Monthly or quarterly audits are point-in-time checks. They confirm that controls were working at the sample moment, not that they have been working continuously. Most fraudulent changes to vendor records happen between the review cycles, in the window where attackers know the master file is trusted and re-verification isn't scheduled. By the time the next audit runs, the fraudulent payment has gone out and the evidence trail may already be cold. Continuous controls close this window by re-verifying on every change, every relevant external signal, and every payment.

How do companies audit AP under a continuous controls model?

Internal audit and external assurance teams move from sampling-based reviews to evidence-based confirmation. Rather than asking "how do you verify vendors?" and accepting a process description, they ask "show me the verification record for these payments" and get an answer in minutes. The audit function still owns assurance, but the evidence base is continuous rather than periodic, and the audit cycle gets shorter because the underlying records are already organised for query.

What to do next

Here are four useful next steps, depending on where you are.

If you want to pressure-test your existing controls. Our guide to pressure testing finance workflows covers how to evaluate whether your current controls would hold under modern fraud conditions. Useful for finance leaders preparing a controls review.

If you want a broader view of the financial controls landscape. Our financial controls guide covers the full control environment finance leaders are responsible for, from segregation of duties to reconciliation and audit.

If you're working on the broader CFO strategy. Our Cybersecurity Guide for CFOs 2026 is an in-depth look at strategy and fraud prevention, including the CFO's role in leading an anti-cybercrime programme.

If you want to see continuous controls in action.Book an Eftsure demo to see how multi-verification layers operate inside the AP workflow. Useful for finance leaders moving from "what is this?" to "what would it look like to implement it?"